In today’s fast-paced financial world, understanding the basics of money management is more important than ever. Opening a savings account is often a key step in beginning your journey to financial independence. For UK residents, a savings account offers a safe, reliable, and interest-generating way to store your hard-earned money while keeping it easily accessible.

This guide is designed to answer the question: “What is a savings account?” and help UK savers make informed financial decisions. From its definition, benefits, pros and cons, alternative options, to frequently asked questions, this article covers it all.

Introduction: The Power of Saving in the UK

Whether you’re setting aside money for a rainy day, a holiday, or long-term financial security, a savings account remains one of the safest and most accessible options for UK residents. But what is a savings account, and how does it fit into your financial journey in 2025?

In this detailed guide, we break down everything you need to know—from how savings accounts work, their benefits, pros and cons, to the best alternatives available in the UK market. Let’s dive in.

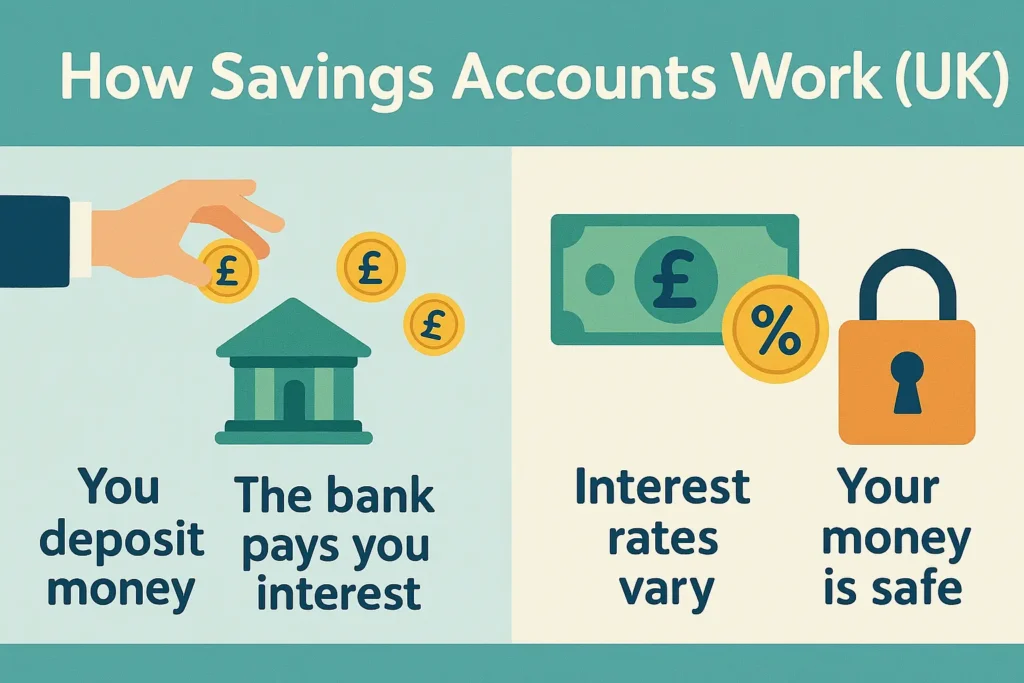

What is a Savings Account?

A savings account is a special type of bank account that helps you save money safely and earn interest on it over time. It’s different from your current account, which you use for day-to-day spending like shopping, bills, or cash withdrawals.

Instead, a savings account is meant for putting money aside, like for a holiday, a car, or an emergency fund.

Example:

Let’s say Emma opens a savings account with Nationwide.

- She puts in £1,000.

- The bank gives her 4% interest per year.

- After one year, she earns £40, just for keeping her money there.

- Now she has £1,040 — without doing anything extra!

The more she saves, the more interest she earns.

UK banks offer a variety of savings accounts, such as:

- Easy Access Savings Accounts

- Notice Savings Accounts

- Fixed-Rate Savings Bonds

- Regular Saver Accounts

How Does a Savings Account Work?

Here’s a breakdown of how savings accounts function in the UK:

1. Opening an Account

You choose a financial provider, select the type of account, and submit your ID and proof of address. Many banks now offer fully digital onboarding.

2. Depositing Money

After opening the account, you can either make a one-time deposit or schedule regular payments. Some regular saver accounts require monthly deposits.

3. Earning Interest

You earn interest on your deposited funds. Interest rates may be:

- Fixed (guaranteed for a term)

- Variable (subject to change)

Interest is typically calculated daily and paid monthly or annually.

4. Accessing Your Funds

- Easy access accounts allow instant withdrawals.

- Notice accounts require prior notice (e.g., 30 days).

- Fixed-term savings accounts keep your money locked away for a certain period of time.

5. Tax Implications

Under the Personal Savings Allowance (PSA):

- Basic-rate taxpayers: Up to £1,000 interest tax-free

- Higher-rate taxpayers: Up to £500

- Additional-rate taxpayers: No allowance

Interest beyond this is subject to income tax.

Key Benefits of a Savings Account in the UK

1. Safe & Secure

UK savings accounts are covered by the Financial Services Compensation Scheme (FSCS), which protects up to £85,000 per person, per institution. This makes it a low-risk option for safeguarding your funds.

2. Earn Interest on Idle Money

Your money doesn’t just sit—it grows. Even if the interest rate is modest, over time, it can lead to significant gains, especially when compounded.

3. Encourages Financial Discipline

By separating spending money (current account) from savings, you reduce the temptation to overspend and create better money habits.

4. Easy Account Access

With mobile banking and online portals, managing and monitoring your savings account is fast, simple, and transparent.

5. Flexibility and Variety

There’s a wide range of savings accounts tailored to your goals—whether it’s short-term access or locking in a higher interest rate.

Pros of a Savings Account

- Low risk: Capital is protected and backed by FSCS.

- Liquidity: Easy access options are available.

- No fees: Most accounts come with zero maintenance charges.

- Simple setup: Accounts can be opened in minutes online.

- Compounding interest: Your interest earns interest over time.

Cons of a Savings Account

- Lower returns: Interest rates may not beat inflation.

- Access restrictions: Some accounts limit how often you can withdraw.

- Rate variability: Variable-rate accounts can fluctuate.

- Introductory rates: Many accounts offer high initial rates that drop after 12 months.

Best Alternatives to Savings Accounts in the UK

While savings accounts are a solid choice, they aren’t always the most rewarding. Here are top alternatives to consider:

1. ISAs (Individual Savings Accounts)

- Cash ISAs: Similar to savings accounts but interest is tax-free.

- Stocks & Shares ISAs: Potential for higher returns, with added risk.

2. Premium Bonds

- Offered by NS&I. Instead of interest, you enter a monthly prize draw. Winnings are tax-free.

3. Fixed-Term Savings Bonds

- Higher interest for locking in funds (1–5 years). Not ideal for those needing quick access.

4. High-Yield Investment Accounts

- Riskier, but potentially more rewarding than savings accounts.

5. Digital-Only Bank Offers

- Some challenger banks like Monzo, Starling, and Atom Bank offer higher rates and app-based management.

Quick Comparison Table

| Feature | Savings Account | ISA | Premium Bonds | Fixed-Term Bond |

| Access | Easy/Notice | Easy | Flexible | Locked-in |

| Interest | 1–5% | Up to 5% | Prize-based | Up to 6% |

| Risk Level | Low | Low-Medium | None | Low |

| Tax-Free? | Up to PSA limit | Yes | Yes | No |

Looking for top-performing savings products? Read our updated guide on the

👉 Best Savings Accounts in the UK

Frequently Asked Questions (FAQs)

1. Is my money safe in a UK savings account?

Yes. Funds up to £85,000 are protected by the FSCS per institution.

2. How much interest can I earn?

The interest rate you receive will vary based on the account type and provider, usually falling between 1% and 5% AER.

3. Can I open a savings account online?

Absolutely. Most UK banks offer online applications that take just a few minutes.

4. What is the difference between a current and savings account?

Current accounts are for daily spending. Savings accounts are designed for storing and growing your money over time.

5. Are savings accounts worth it in 2025?

Yes, especially when paired with tax-free options like ISAs or used alongside investment strategies.

Disclaimer

This article is for informational purposes only and does not constitute professional financial advice. Always consult with a certified financial adviser before making any financial decisions.

Conclusion: Is a Savings Account Right for You?

A savings account remains one of the most reliable tools for growing your money safely. With the UK offering a broad spectrum of account types, from easy-access to fixed-rate, there’s a suitable option for every financial need and goal. Whether you’re just starting out or looking to optimise your savings in 2025, understanding how these accounts work—and comparing them to other products—is the first step towards financial empowerment.

📖 Want to explore further? Don’t miss our article on 👉 Best Savings Accounts in the UK